Education Department Finalizes Student Loan Caps and Repayment Overhaul

Education Department Finalizes Student Loan Caps and Repayment Overhaul

The rule phases out Grad PLUS, creates new repayment options and puts a $409 billion taxpayer-savings claim at the center of the fight.

WASHINGTON - The U.S. Department of Education finalized a sweeping student-loan rule that will cap federal borrowing for graduate students, professional students and parents while replacing much of the current repayment system beginning July 1, 2026, according to a final rule published Friday in the Federal Register.

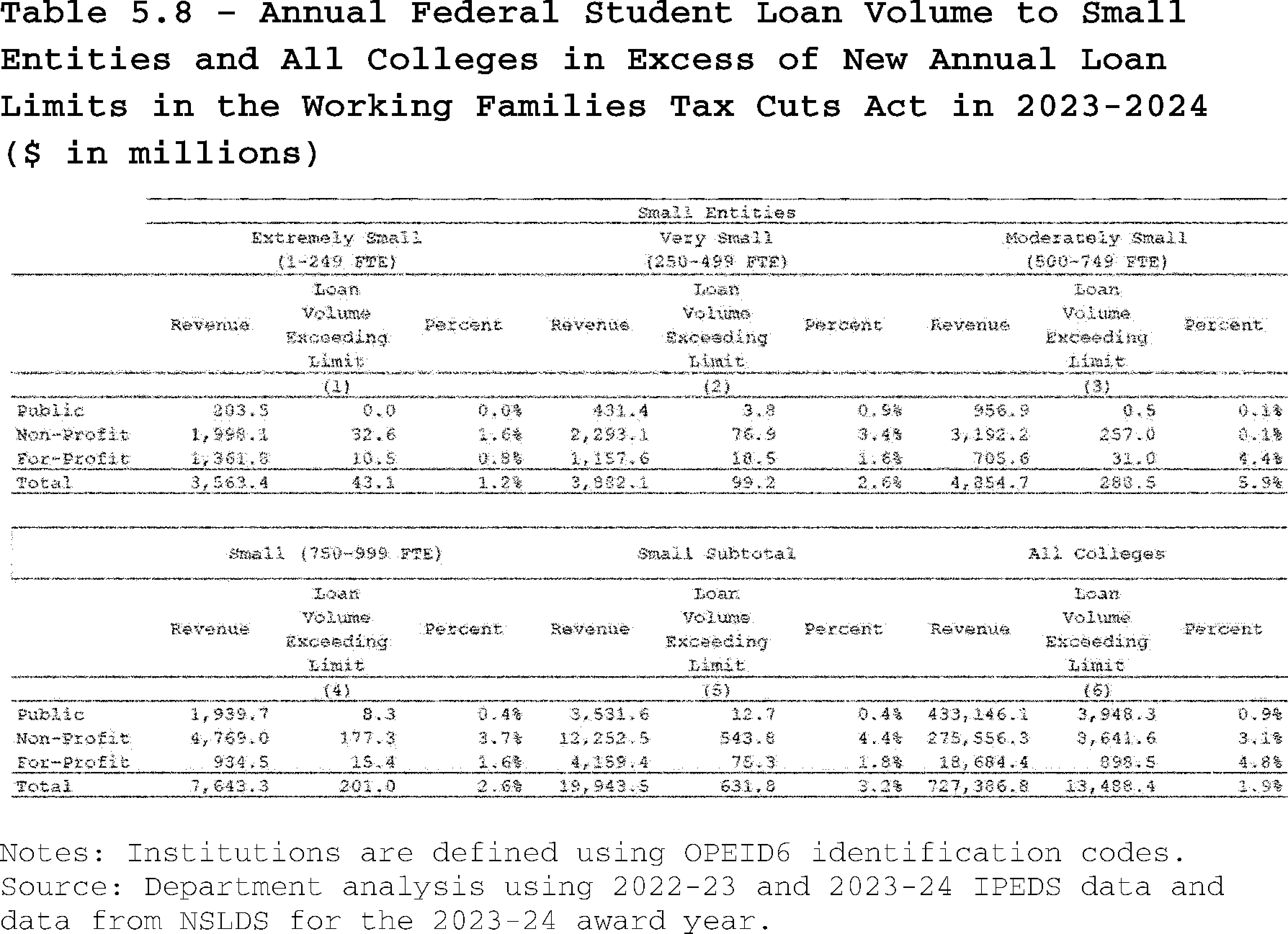

The rule, listed as 91 FR 23768 under Docket ID ED-2025-OPE-0944 and RIN 1840-AD98, implements student-loan provisions in Public Law 119-21, the Working Families Tax Cuts Act. The Department said the package will reduce federal student-loan debt by $224 billion and produce $409 billion in taxpayer savings compared with its budget baseline.

The fight now turns from Congress to implementation. Borrowers will have to sort through new loan limits, schools will have new authority to set program-level caps and financial-aid offices will have less than 14 months to prepare for the first July 2026 deadline.

The Story So Far

Congress changed the loan program through Public Law 119-21, which President Donald Trump signed on July 4, 2025, according to the Federal Register notice. The Education Department said the law directed the agency to amend regulations under title IV of the Higher Education Act for Federal Perkins Loans, Federal Family Education Loans and Direct Loans.

The Department convened the Reimagining and Improving Student Education Committee for negotiated rulemaking sessions in September, October and November 2025, according to the agency's April 30 release. The Department said the committee included higher education institutions, student-loan borrowers and taxpayer organizations, and that the group reached consensus on the package.

The agency published a proposed rule on Jan. 30, 2026, then received more than 80,000 public comments, according to the Department. The final rule now sets the legal framework for a phased rollout that starts next summer and continues into 2028.

What's Happening Now

The final rule eliminates the Graduate PLUS program for future borrowers and establishes new annual and aggregate loan limits. The Department's negotiated rulemaking release said new graduate borrowers will be capped at $20,500 annually and $100,000 in aggregate graduate borrowing beginning in July 2026. Professional students will be capped at $50,000 annually and $200,000 in aggregate borrowing, according to the same agency release.

The Federal Register notice says the rule also creates a lifetime federal student-loan cap of $257,500 for most borrowers. The Student Borrower Protection Center said Parent PLUS loans for new borrowers will be capped at $20,000 per year and $65,000 total per child after July 1, 2026, a change from the previous structure that allowed parents to borrow up to the cost of attendance minus other aid.

The repayment overhaul is just as large. The Department said the rule phases out existing Income-Contingent Repayment plans, creates a Tiered Standard plan and establishes the Repayment Assistance Plan, an income-driven option. The Department said RAP payments will count toward Public Service Loan Forgiveness if borrowers meet the program's other requirements.

The Student Borrower Protection Center said borrowers with new loans after July 1, 2026, will generally have two repayment choices: the new standard plan or RAP. Its borrower summary said RAP requires payments from 1 percent to 10 percent of adjusted gross income, includes a $10 monthly minimum and reduces monthly payments by $50 per dependent child.

Chart via Federal Register / Government Publishing Office (public domain)

Chart via Federal Register / Government Publishing Office (public domain)

The Conservative View

Administration officials frame the rule as a correction to years of unlimited borrowing, tuition inflation and repayment complexity. The Education Department said graduate students hold more than one-third of federal student-loan debt, while citing outside research that 40 percent of master's degree programs have a negative return on investment.

"The Trump Administration is focused on putting students and taxpayers first, which is why we are implementing durable policies to make higher education more affordable."

Nicholas Kent, Under Secretary of Education

Kent said the law addresses tuition costs, unchecked borrowing and repayment options that left some borrowers with higher balances despite making payments. The Department also said the rule allows institutions to establish programmatic loan caps tied to the value of academic programs, a policy the agency says can prevent overborrowing in programs with lower earnings or higher default rates.

Supporters of the fiscal argument point to the Department's budget estimate. The agency said the rule produces a net budget impact of negative $409.3 billion from loan cohorts 1994 through 2035, excluding the professional-student definition, and a separate $537 million impact for the professional-student definition across loan cohorts 2027 through 2036.

The Progressive View

Democrats and borrower advocates argue the same caps could push students and parents away from federal loans and toward private lenders with fewer protections. House Education and Workforce Committee Democrats said in March that more than 85 members opposed the proposed rule because they believed the structure would restrict access to higher education.

"We are concerned that this new structure of federal graduate lending will further restrict higher education access, particularly for low- and middle-income borrowers."

House Education and Workforce Committee Democrats, March 2026 comment letter

The Student Borrower Protection Center said eliminating Grad PLUS without lowering college prices could force families into expensive private loans. The group said current Grad PLUS borrowers may continue borrowing for the remainder of their program or up to three academic years, whichever is shorter, but new students entering after July 1, 2026, will lose access to the program.

House Democrats also criticized the repayment changes. In their March statement, the members said the law restricts access to federal aid and eliminates affordable repayment plans, and they urged the Department to evaluate how each implementation decision would affect students' ability to pay for college.

Other Perspectives

Colleges and financial-aid offices now sit in the middle of the rollout. The Education Department said institutions may set lower programmatic loan caps, which could give schools more control over borrowing levels but also require them to justify limits to students planning graduate or professional degrees.

Independent budget analysts will likely focus on the difference between federal savings and household costs. The Department's $409 billion estimate measures federal budget impact against a baseline. It does not mean borrowers immediately save that amount, and it does not resolve whether families facing capped federal loans will reduce enrollment, pay out of pocket or use private credit.

Economic Implications

The clearest economic mechanism is a credit-rationing shift. The Department is reducing open-ended federal credit for graduate, professional and parent borrowers, while giving schools some authority to set lower limits. If tuition prices do not fall with borrowing capacity, affected students may face three choices: choose lower-cost programs, use private loans or skip programs whose costs exceed federal limits.

The taxpayer case rests on the Department's estimate of a negative $409.3 billion budget impact, plus its claim that reduced overborrowing lowers student-loan debt by $224 billion. The agency also estimated annualized paperwork burden between $25.0 million and $37.2 million, administrative systems costs between $10.4 million and $12.1 million, system maintenance and operation costs between $7.4 million and $7.8 million, and staffing costs between $5.5 million and $6.0 million at 3 percent and 7 percent discount rates.

For households, the main cost question is distribution. The Student Borrower Protection Center said RAP can run for 30 years before cancellation, longer than several previous income-driven repayment paths. The Department counters that RAP eliminates negative amortization, meaning unpaid interest not covered by monthly payments will not cause balances to grow under the plan.

Photo by Rica Rentutar, via Wikimedia Commons (CC BY 4.0)

Photo by Rica Rentutar, via Wikimedia Commons (CC BY 4.0)

By the Numbers

- $20,500 - Annual federal loan cap for new graduate borrowers, according to the Education Department.

- $50,000 - Annual federal loan cap for new professional-student borrowers, according to the Education Department.

- $257,500 - Lifetime federal student-loan cap for most borrowers, according to the Federal Register notice.

- $409.3 billion - Estimated federal budget impact, according to the Education Department's final rule.

- More than 80,000 - Public comments received after the Jan. 30 proposed rule, according to the Department.

What People Are Saying

"The Secretary amends the regulations for the Federal student loan programs authorized under title IV of the Higher Education Act (HEA) of 1965, as amended (the title IV, HEA programs) to implement the statutory changes to the title IV, HEA programs included in Public Law 119-21."

Federal Register final rule

"The final rule includes four key provisions: Eliminates the Grad PLUS program to help curb tuition growth by ending unlimited borrowing; establishes reasonable annual and aggregate loan limits for graduate and professional students; allows institutions to establish their own programmatic loan caps that match the true value of their academic programs; and simplifies student loan repayment by creating a new Tiered Standard plan and establishing a new income-driven repayment plan known as the Repayment Assistance Plan."

U.S. Department of Education

"Graduate PLUS loans are eliminated for new students on July 1, 2026. Current students are permitted to borrow Graduate PLUS loans for up to three years."

Student Borrower Protection Center

"We urge the Department to put students and borrowers first and consider how each decision will impact a student's ability to afford their education."

House Education and Workforce Committee Democrats

The Big Picture

The first date to watch is July 1, 2026, when most loan-limit and repayment provisions take effect, according to the Education Department. The agency said rehabilitation, deferment and forbearance provisions take effect July 1, 2027, while certain repayment-plan sunsets arrive July 1, 2028.

The political fight is unlikely to end with publication. Borrower advocates may challenge implementation choices, colleges may seek guidance on programmatic caps and lawmakers may test whether the rule is vulnerable under the Congressional Review Act. For students making graduate-school or parent-borrowing decisions this year, the practical question is simpler: whether the federal loan system they expected will still be available when their next academic year starts.